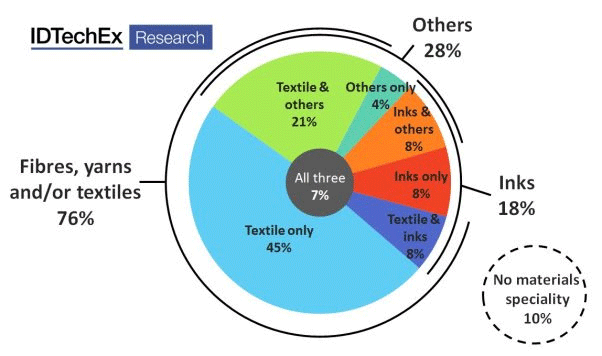

Whilst the majority of wearable technology products sold today still fit with the components-in-a-box design, 2015 has been a record year for investment in smart clothing and e-textile products. To reach the masses, wearable technology must be useful, practical and fashionable, and seamless integration within textiles and clothing is seen as a key part of this. However, with many challenges, not least around washability, durability and in manufacturing, the majority of projects over the last decade were restricted to low volume niche products. This is now changing.

IDTechEx’s most recent work in the area found the market for pure e-textiles to be worth $100m in 2015. Much of the attention focuses around products in the ‘Sports & Fitness’ sector and notably compression wear in the form of a ‘Smart Shirt’ or otherwise. However, whilst many of the largest players focus here, there is significant activity across verticals including military, medical & healthcare, workwear and others which are all described in detail within the new market research report “E-Textiles 2016-2026”.

The impact of the large companies entering the space will have a significant effect. Whilst this includes entries from many large apparel brands like Adidas, UnderArmour and Nike, many other entries elsewhere in the value chain have had significant impact. Materials companies like DuPont, Nagase/EMS, Hitachi Chemical and others now offer specialised electronic materials for apparel. Electronics manufacturing services giants like Flex and Jabil are invested heavily, the latter having acquired leading integrator Clothing+ in 2015. Finally, there is a wave of interest from Asia, where textiles giants from India, Sri Lanka, Taiwan and China are now entering the market with large ambitions and deep pockets. The value chain is assembling and volume production will soon be possible for a variety of diverse products.

Whilst the focus around ‘Smart Shirt’ biometric products has been undeniable, the breadth of applications includes tracking specific physiological conditions (beyond heart and respiration rate), to the introduction of heaters, haptics, or other actuators for rehabilitation or comfort, to the optimisation of data and power wiring within military apparel, to the integration of lighting or other visual features in apparel and home textiles alike.

This report describes the entire e-textile ecosystem, starting from the bottom up with detailed study of the material options and suppliers. At the component level, the report describes major players and techniques for all of the main options including: motion, touch, pressure, and electrical sensors, heating/cooling, lighting, communication and connectors. Examples of new technologies which remain in research at the moment, but will reach maturing in the coming years are also described including e-fibres (RFID, sensing and more); new materials like graphene, nanotubes and alike; energy harvesting including photovoltaic, piezoelectric and triboelectric options; energy storage in batteries and supercapacitors, and even logic and memory.

The report concludes that the market for e-textiles will reach over $3bn by 2026, from around $100m in 2015. With forecasts split by product and sector, details of all of the technology types, key players and market trends and finally over 25 full company profiles based on IDTechEx’s interview-based primary research, “E-Textiles 2016-2026” provides the most comprehensive overview of the electronic textiles industry today.

{kind=link}